Everyone Wants a Slice

8 July 2026 · 8 min read

Milan Bilimoria

Milan BilimoriaThere is a version of early-stage company building that most founders recognise. You have a product, an idea, or the early shape of both. You join an accelerator to get structure and a small cheque. You bring on an advisor who knows the industry. Then another one who has good investor connections. A third who offers to make introductions. A co-founder who seems right at the time but leaves six months later.

None of those decisions felt like major equity events. They felt like the normal costs of getting a company off the ground: small percentages in exchange for help, support, credibility, and momentum. The accelerator gave you £60k and a cohort of peers. The advisors gave you their time and their networks. The co-founder gave you eighteen months before the relationship broke down.

What they also gave you, cumulatively, is a cap table that arrives at your first institutional raise already carrying the weight of every one of those decisions. And in a market where pre-seed and seed capital is harder to access than it has been at any point in the last decade, that weight compounds in ways most founders have not modelled.

This piece is about what that equity actually costs, modelled precisely, and what the cap table looks like for a founder who gave away a reasonable amount before their first raise versus one who did not.

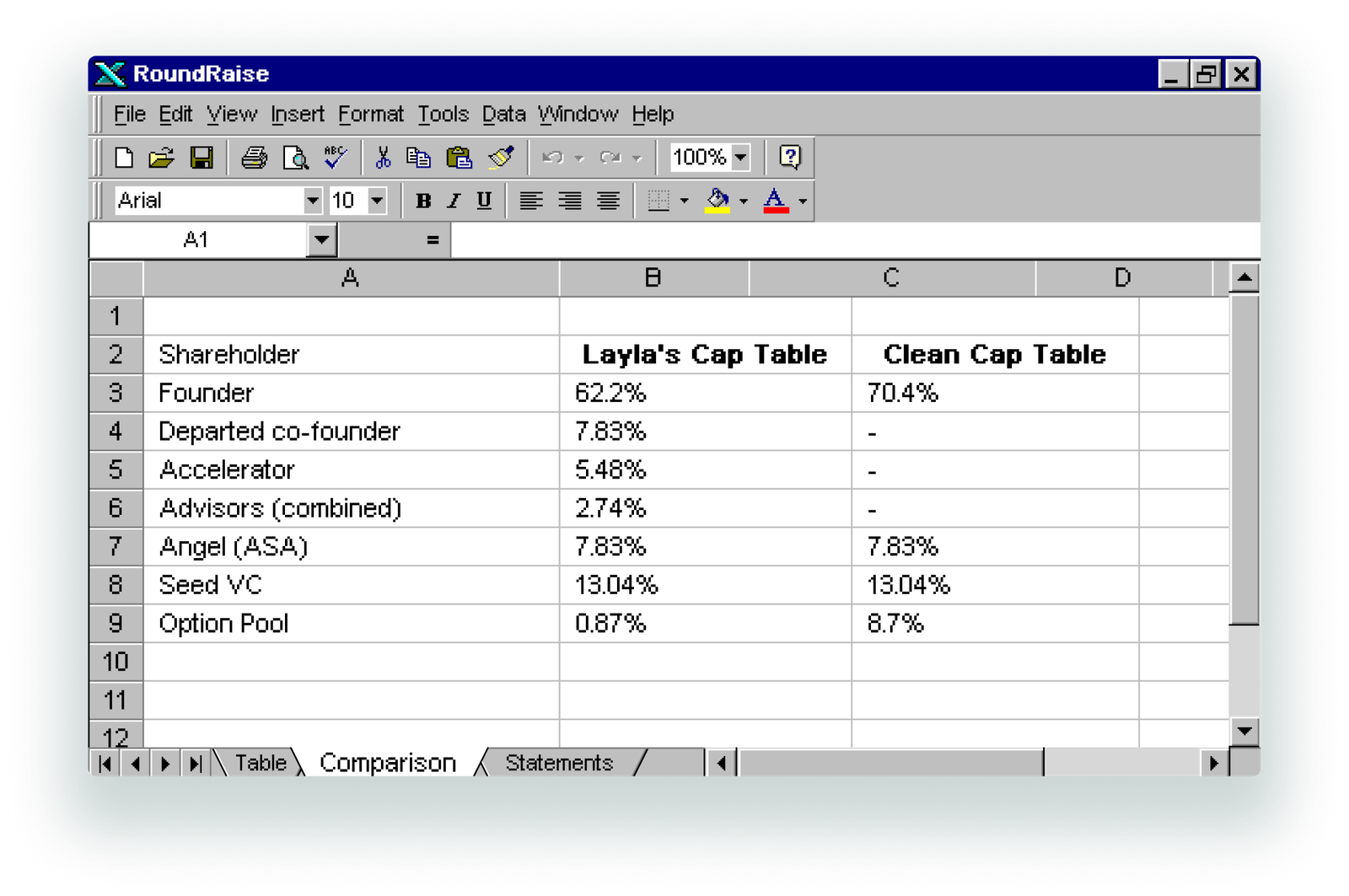

Layla’s cap table before she raises a penny

Layla starts with 100% of her company. Over the eighteen months between incorporation and her first institutional raise, the following happens.

She gets accepted into a UK accelerator programme. Typical UK accelerator programmes take between 5% and 10% equity in exchange for cheques ranging from £50k to £150k. Layla’s accelerator takes 7% for £60k, which is in line with market standard. She accepts because the network, the mentorship, and the credibility of the programme are worth the dilution, and at the time, 7% feels like a reasonable price for what she is getting.

At this point Layla owns 93% of her company. She has received £60k. The accelerator owns 7%. This feels fine.

She brings on three advisors across the following six months. An industry veteran who can open doors with potential enterprise customers takes 2% with no vesting clause, because the conversation moved quickly and the paperwork felt like a formality. A former operator from a relevant sector takes 1% with a two-year vesting schedule. An angel introducer who promises to connect her with investors takes 0.5%, also unvested.

The total advisor pool should be no more than 5% of total company equity across all advisors, and advisor equity should always vest. Layla’s three advisors together hold 3.5%, which is within that range. But two of the three grants have no vesting, which means both advisors own their equity outright from day one regardless of whether they deliver anything.

Layla now owns 89.5% of her company. She has given away 10.5% across an accelerator and three advisors before a single institutional investor has looked at her cap table. Each individual decision felt reasonable. The cumulative effect is a different calculation.

Then her co-founder leaves. They joined eighteen months earlier, worked hard for six months, and then the relationship deteriorated. There was no vesting agreement in place when the equity was split, which was a decision made in the optimism of founding rather than with any view to what happens if the partnership does not work. The co-founder holds 10% of Layla’s company. They are no longer working on it. They have no legal obligation to return any of it. It sits on the cap table as dead equity: a permanent fixture that represents neither contribution nor value to the company going forward, but that will dilute every subsequent investor, appear on every cap table shared in every data room, and reduce Layla’s ownership at every future round.

Layla now owns 79.5% of her company. She has raised £60k. She is ready to raise her first proper round.

What the cap table looks like at seed close

Layla raises a £150k ASA at a £1.5m post-money cap, followed by a £600k seed round at a £4m pre-money valuation with a 10% option pool created pre-money. Both rounds are structured identically to a founder with a clean cap table.

The difference is not in the terms of the rounds. It is in the starting point.

Working from 1,000,000 shares at founding:

-

Layla: 795,000 shares

-

Departed co-founder: 100,000 shares

-

Accelerator: 70,000 shares

-

Advisors (combined): 35,000 shares

At seed close, after the option pool expansion, ASA conversion, and seed investment:

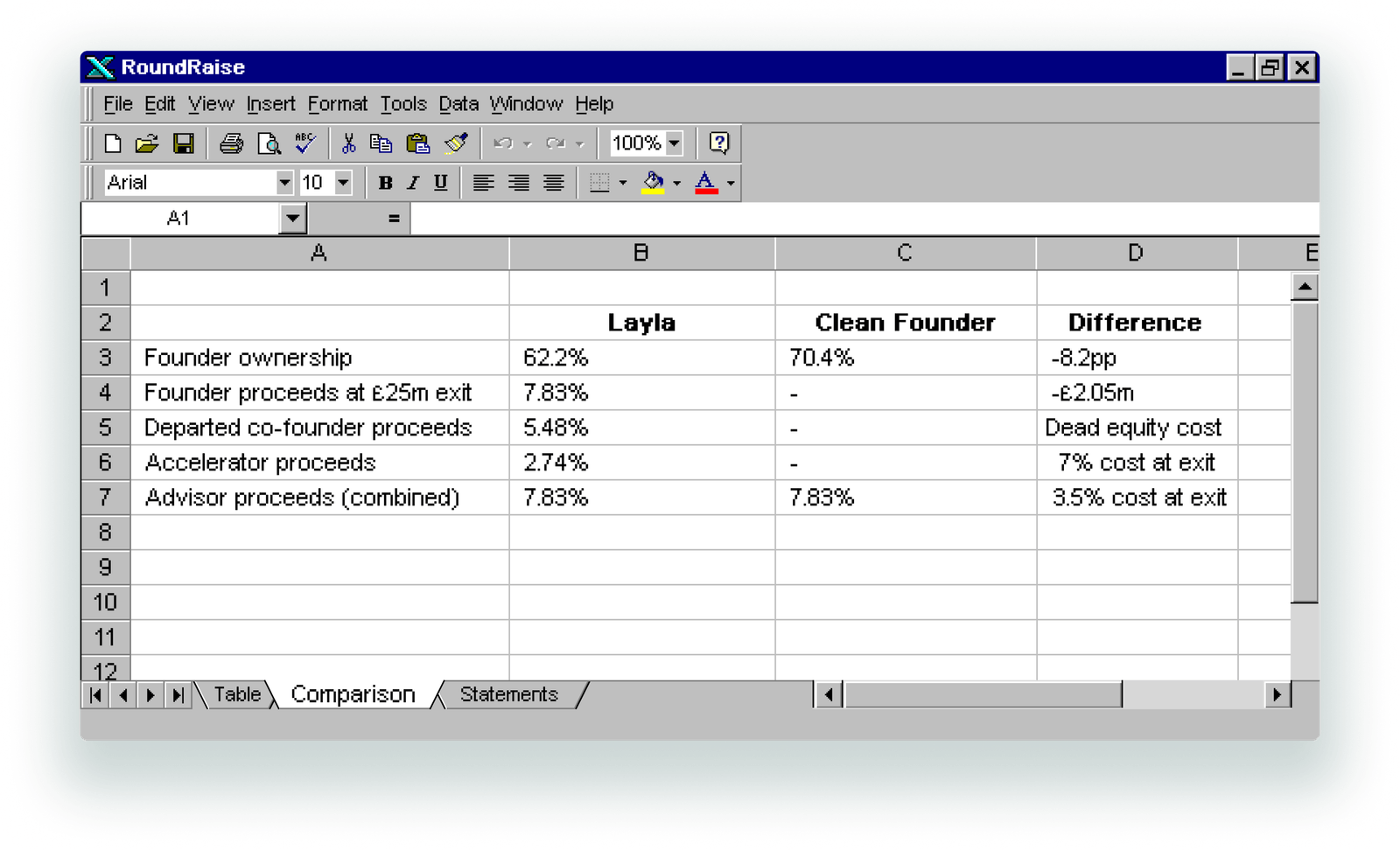

Layla owns 62.2% of her company after the seed round closes. A founder who raised identically, on the same terms, from the same investors, but without the pre-raise equity grants, owns 70.4%.

The gap is 8.2 percentage points. It does not sound enormous. But it arrived entirely from decisions made before Layla had a single investor conversation. The accelerator, the advisors, the departed co-founder: none of those equity events felt like they were reducing her seed round outcome. They were.

The departed co-founder’s 7.83% stake is the most significant single item on Layla’s cap table that is producing no value. It is larger than the angel investor’s stake, larger than each advisor’s stake, and it sits there permanently unless Layla has the legal mechanism and the negotiating leverage to buy it back, which at this stage of the company she may not.

What this costs at exit

At a £25m exit, the 8.2 percentage point gap between Layla’s ownership and a clean-cap-table founder’s ownership translates directly into proceeds.

The gap is £2.05m. That is the combined cost of the pre-raise equity decisions: the accelerator’s 7%, the three advisors’ 3.5%, and the departed co-founder’s 10%. Each one was a reasonable decision in isolation. Together, across a 29-month journey from seed to exit, they cost Layla £2.05m.

Imagine handing someone a £2m cheque on the day you sign your exit documents. That is what the cumulative effect of those equity grants looks like at a £25m exit. Not in a single dramatic moment, but spread across a series of decisions that each felt small at the time.

The accelerator’s contribution is the most defensible of the three. Top-tier UK accelerator alumni raise follow-on funding at rates above 74% within three years, which suggests the network and credibility effects are real. If the accelerator genuinely accelerated Layla’s path to the seed round, the 7% may be worth it on a risk-adjusted basis. The question is not whether to join an accelerator but whether the specific terms, the equity percentage, the vesting structure, and the implied valuation, reflect a rational assessment of what the programme is worth to you rather than an acceptance of whatever was offered.

The advisor grants are harder to defend on the numbers. The median advisor equity grant at pre-seed was 0.21% in H1 2024, and only 10% of pre-seed advisors received 1% or more. Layla gave 2% to a single advisor without a vesting clause. Market standard would have been 0.25% to 0.5% with a two-year vesting schedule. The difference between market standard and what Layla agreed to is not a rounding error at exit.

The departed co-founder is the clearest lesson. Dead equity is not a metaphor. It is a real number on a real cap table that reduces every existing shareholder’s ownership at every subsequent dilutive event and produces nothing in return. The mechanism that prevents it is a co-founder vesting agreement with a cliff period, signed at founding before either party has any reason to anticipate the relationship breaking down. It is one of the cheapest legal documents a founder can produce and one of the most consistently overlooked.

What a clean cap table looks like instead

None of the above is an argument against accelerators, advisors, or co-founders. It is an argument for treating every equity grant as a financial decision rather than a relationship decision, and for having the same rigour about pre-raise equity that most founders develop, too late, about their term sheets.

A clean cap table entering a seed round does not mean a founder who raised alone with no support. It means a founder who modelled the long-term cost of each equity grant, negotiated terms that reflected market standard, insisted on vesting for every grant including co-founder equity, and understood what the cumulative effect of those decisions would look like at the moment of exit.

The accelerator that takes 4% instead of 7% on the same terms is not necessarily worse than the one that takes 7%. The advisor who accepts 0.25% with a two-year vesting schedule is not less committed than the one who takes 2% unvested. The co-founder vesting agreement does not signal distrust; it signals that both parties understand what they are agreeing to and what happens if circumstances change.

These are conversations most founders do not have because the pre-raise period feels like the wrong time to be legalistic about equity. It is, in fact, the only time those conversations are free. Once the cap table is set and the shareholders are in place, the cost of fixing it is measured in legal fees, negotiation time, and the goodwill of people who have no particular incentive to give equity back.

At RoundRaise, we build tools that help founders model the long-term cost of every equity decision, from the first grant to the final waterfall. If you want to see what your current cap table looks like at different exit scenarios, you can find us atroundraise.co.uk.

We also have a founder wall atapp.roundraise.co.uk/board, a space where founders leave the things they wish they had known earlier. If you have given away equity you later regretted, it belongs there.