Is the Pre-Seed Round Dead?

29 April 2026 · 5 min read

Milan Bilimoria

Milan BilimoriaSomething has shifted in how early-stage founders are getting their first capital, and it has happened gradually enough that most people building companies right now have not stopped to examine what it means for them structurally.

The institutional pre-seed round, a single cheque from a micro-VC or early-stage fund that sets clean terms, establishes a lead investor, and gives a founder a clear cap table to take into their next raise, is not disappearing. But it is concentrating. According to Carta’s State of Pre-Seed data, the number of pre-seed instruments issued fell 13% in 2025 compared to 2024, and the decline in rounds above $1 million was sharper still: Q1 2024 had roughly 2,900 rounds above that threshold, while Q1 2025 had only 1,700. The capital that remains is flowing to fewer companies, typically those with more traction, stronger networks, or both.

For the majority of first-time founders sitting outside that narrowing pool, the practical reality is different. They are raising through angels: multiple smaller cheques, signed at different times, on different terms, from investors who often have no formal relationship with each other and no obligation to lead a future round. This is not a new phenomenon, but it has become the default route rather than the exception. UK angel investors now participate in 92% of pre-seed rounds globally, a figure that reflects broader trends rather than the UK specifically, but one that directionally captures what is happening here. The institutional pre-seed is for a shrinking subset of founders. Everyone else is stacking angels and figuring out the implications later.

The problem is that most founders doing this are not modelling what it means for their cap table, and the implications compound in ways that only become visible at the worst possible moment.

The terms problem nobody talks about

When a founder raises through a single institutional investor at pre-seed, the terms of that raise are typically negotiated with some degree of structure on both sides. The investor has a standard instrument, a considered valuation, and an incentive to set terms that work for the next round because they intend to be in it. That does not mean institutional terms are always founder-friendly, but they tend to reflect a coherent view of what the company is worth and what the round should look like.

Angel stacking produces something different. Each cheque arrives with its own terms, set in a separate conversation, often without either party having full visibility of what the other angels in the stack have agreed to. The founder is not negotiating a round; they are negotiating a series of bilateral agreements that will eventually sit on the same cap table and convert at the same Series A. The terms that get set in those individual conversations, particularly the valuation cap, have a direct and permanent effect on how much of the company the founder retains through to exit.

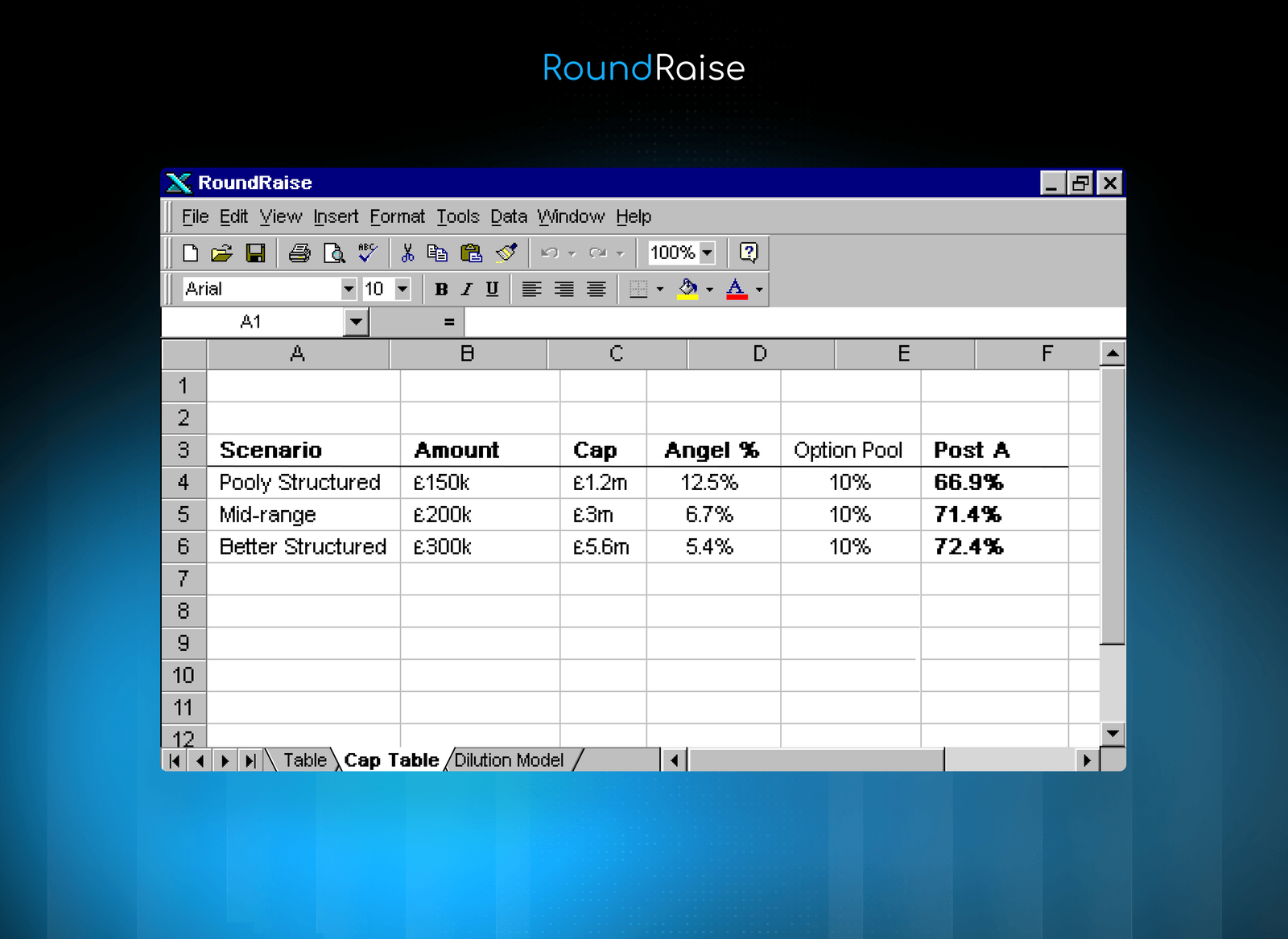

The data from our own conversations with founders illustrates this clearly. We have spoken to founders raising at caps as low as £1.2m for £150k, and founders raising at £5.6m for £300k. Both are angel-stacked pre-seed raises. Both will sit on a cap table alongside a future Series A. But the founder ownership outcomes they produce are not even close to each other, and neither founder, at the time of signing, had modelled what their cap table would look like at Series A conversion.

What the numbers actually show

To make this concrete, we modelled three scenarios based on real conversations with founders in our network. All three are angel-stacked pre-seed raises with a single SAFE instrument, followed by a £1.5m Series A at an £8.5m pre-money valuation, with a standard 10% option pool created pre-money at Series A.

The table below shows what each founder actually owns after the Series A closes.

The difference between the first and third scenario is 5.5 percentage points of founder ownership, produced entirely by the valuation cap agreed at pre-seed. At a modest exit of £30m, that gap represents roughly £1.65m in founder proceeds. At a larger exit it compounds further. And this is modelling a single SAFE instrument per founder; founders who have stacked multiple SAFEs at different caps face a more complex version of the same problem, with each instrument contributing its own dilutive effect at conversion.

The point is not that angel stacking is the wrong route. For most first-time founders right now, it is the only realistic route to early capital. The point is that the terms agreed in those individual conversations are not administrative details to be sorted later. They are structural decisions with permanent consequences, and they deserve the same level of modelling that a founder would apply to any other significant financial commitment.

Why this is getting worse, not better

The concentration of institutional pre-seed capital is not a temporary market condition. It reflects a structural shift in how early-stage funds are operating: larger fund sizes require larger cheque sizes to deploy capital efficiently, which pushes minimum investment thresholds up and leaves a widening gap at the sub-£500k raise level. That gap is being filled by angels, by SEIS funds writing smaller cheques, and by founders raising across a longer timeline in smaller tranches.

None of that is inherently problematic. Angels provide capital, networks, and in many cases genuinely useful operational experience. SEIS tax relief makes early UK investment more attractive to individual investors than almost anywhere else in Europe. The ecosystem at the sub-institutional level is active and, in some sectors, well-developed.

What is missing is the structural rigour that institutional investors bring by default. When a fund leads a pre-seed round, they model the cap table. Their lawyers draft the instrument. Their partners have seen hundreds of similar rounds and have a calibrated view of what fair terms look like. When an angel writes a £75k cheque into a founder’s SAFE, none of that infrastructure exists on either side of the table. The founder is often drafting or accepting a document they do not fully understand, at a valuation they have not stress-tested, with implications they have not modelled. And they are doing it repeatedly, with each new angel who comes into the stack.

The pre-seed round is not dead. But the version of it that most founders are actually doing in 2025 is structurally more complex, more consequential, and less well-understood than the institutional round it has quietly replaced. That gap is worth taking seriously before the Series A conversation begins.