SAFE, Convertible Note, or ASA: Which One Are You Actually Signing?

10 June 2026 · 11 min read

Milan Bilimoria

Milan BilimoriaAt some point before your first raise closes, someone will ask you which instrument you are using. If you have done any reading on early-stage fundraising, you will have encountered all three: the SAFE, the convertible note, and the ASA. They are all described as ways to raise capital without setting a valuation. They all defer the equity conversation to a future priced round. And they are frequently discussed as if they are three versions of the same thing, which they are not.

Two of them are. One of them is meaningfully different, and the difference matters in a way that only becomes visible when the company is under pressure and the clock is running.

This piece is about what each instrument actually does, how the numbers compare at conversion, and why the choice between them is not primarily a mechanical question for UK founders. It is a structural one.

What all three instruments have in common

Before getting into the differences, it is worth being precise about what SAFE, convertible note, and ASA actually share, because the common ground is substantial enough that the confusion between them is understandable.

All three defer the valuation conversation. Rather than agreeing a price per share today, you agree that the investor’s capital will convert into equity at a future priced round, typically at a discount to whatever price that round sets or at a valuation cap, whichever produces a lower conversion price and therefore more shares for the investor. All three are used at pre-seed and seed stage to raise capital quickly, without the legal overhead of a full priced round, and without forcing a valuation discussion before the company has enough data to have that conversation from a position of strength.

Think of all three as an IOU that says: give me money now, and when the company does a proper fundraising round later, I will convert that money into shares at a price that rewards you for taking the early risk. The question is what the IOU costs you in the meantime.

All three can include a valuation cap, a discount, or both. The valuation cap sets a ceiling on the price at which the instrument converts, protecting the investor if the company’s valuation grows significantly before the next round. The discount gives the investor a percentage reduction on the Series A price per share as a reward for investing early. When both exist in the same instrument, the investor converts at whichever produces the lower price per share, which means whichever gives them more shares.

That is the common ground. What separates the three instruments is what happens between the signing date and the conversion date, and what the investor can do if that conversion never comes.

The SAFE: simple, clean, no maturity date

The SAFE, which stands for Simple Agreement for Future Equity, was created by Y Combinator in 2013 specifically to remove the complexity that convertible notes introduced into early-stage fundraising. It is not a debt instrument. It carries no interest rate, no maturity date, and no obligation on the company to repay anything if a priced round never materialises. The investor is making a bet that the company will raise again, and if it does not, the SAFE simply sits on the cap table indefinitely without creating legal pressure on the founder.

The mechanics at conversion are straightforward. If you raise £300k on a post-money SAFE with a £3m cap, the investor owns 10% of the company on a fully diluted basis from the moment of signing. That percentage is fixed. It does not change regardless of what else happens to the cap table between signing and conversion. When the Series A closes, the SAFE converts at the cap price, new shares are issued to the investor, and the percentage they receive reflects the fixed ownership agreed at signing, adjusted for any dilution from the option pool and the new round.

You agree today that the investor owns 10%. That number is written down and does not move. Whatever happens between now and the Series A, the investor’s slice of the pie was set the moment you both signed.

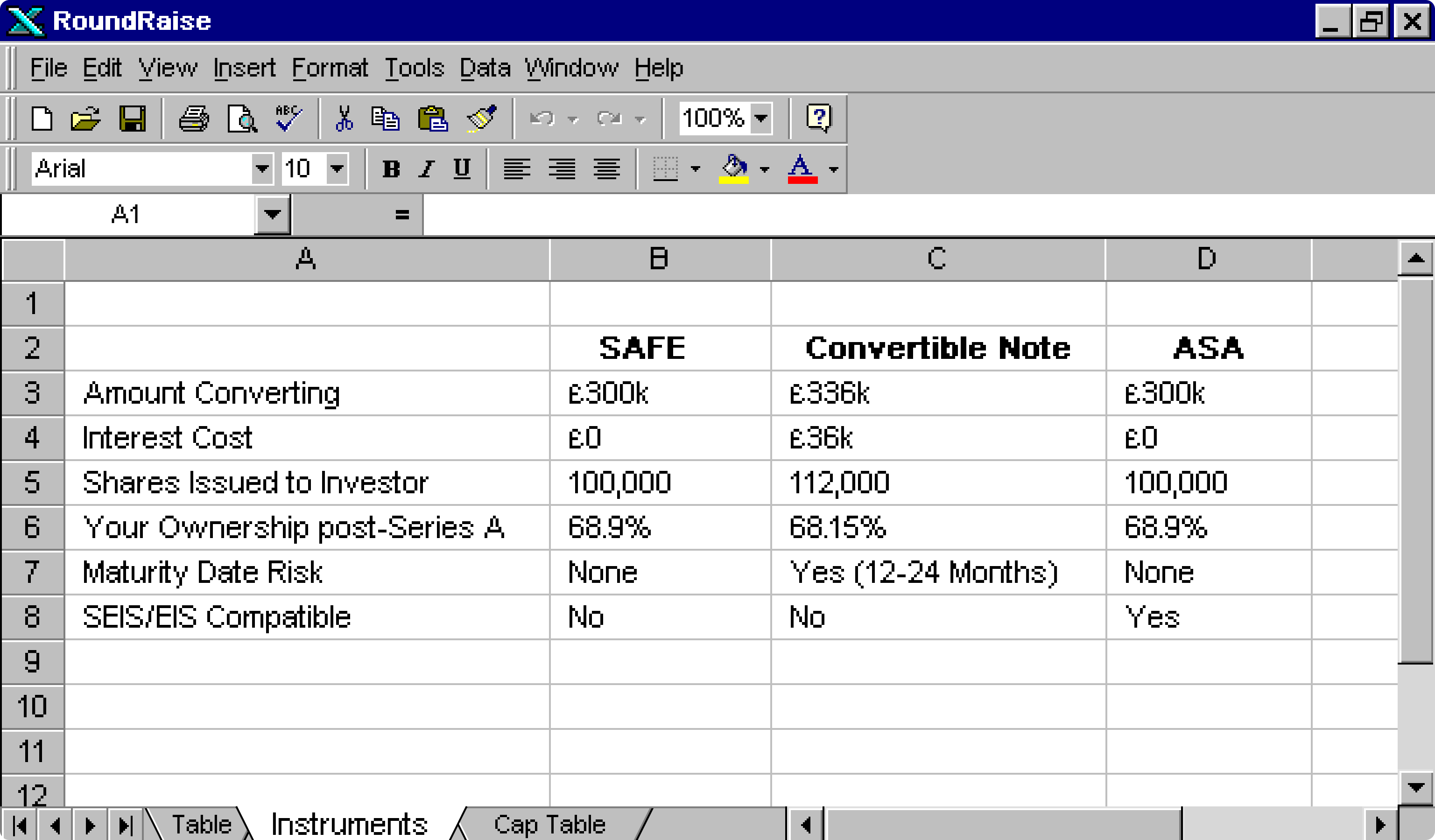

In the scenario we modelled, a £300k SAFE with a £3m cap converting at a £8m pre-money Series A with a 10% option pool, your ownership post-Series A is 68.9%. The SAFE investor holds 6.89%. The numbers are clean because there is nothing accruing in the background between signing and conversion.

The convertible note: debt with a clock attached

A convertible note is structurally different from a SAFE in one fundamental way: it is a loan. The investor is lending you money, and that loan accrues interest at an agreed rate until it converts into equity. The UK Government’s Future Fund used 8% as its benchmark interest rate for convertible notes, which reflects the broader market standard for UK early-stage deals. That rate is applied to the principal amount across the period between signing and conversion, and the total that converts at the next round is not the original investment but the original investment plus accrued interest.

Imagine borrowing £300 from a friend who charges you 8% a year. After 18 months you do not owe them £300 anymore. You owe them £336. When the note converts, it is the £336 that turns into shares, not the £300 you originally received.

In our scenario, £300k at 8% interest over 18 months accrues £36k of interest, bringing the total converting amount to £336k. At the same £3m cap, that converts into 112,000 shares rather than the 100,000 the SAFE investor receives. Your ownership post-Series A is 68.15% rather than 68.9%. The difference is 0.75 percentage points, which at a £30m exit is worth approximately £225k in founder proceeds. It is not catastrophic. But it is a permanent and entirely avoidable cost that compounds further if multiple convertible notes are stacking on the same cap table.

The more significant difference is not the interest. Convertible note terms are tightening in 2025, with interest rates rising by 200 to 300 basis points and discount rates climbing as high as 10.5 percentage points in larger deals. But even at standard terms, the maturity date is the structural feature that changes the nature of the instrument entirely. A convertible note has a fixed maturity date, typically 12 to 24 months from signing, by which point the note is expected to have converted in a priced round. If that round does not arrive before the maturity date, the investor has the legal right to demand repayment of the principal plus accrued interest in cash.

The SAFE says: if the next round never comes, we wait. The convertible note says: if the next round never comes by this date, you owe me the money back. That is a fundamentally different obligation to be carrying when the fundraising environment gets difficult.

For a founder whose Series A takes longer than expected, which in the current UK market, where seed to Series A averages 29 months, is an increasingly common outcome, a convertible note signed with an 18-month maturity date creates a legal obligation that arrives before the problem it was meant to solve has been resolved. The options at that point are to repay cash the company may not have, to negotiate an extension with the investor, or to do a rushed bridge round to convert the note before it matures. None of those options are positions of strength.

Convertible instruments held steady in Q1 2025, but the terms are shifting in favour of investors. In a market where founders already have less leverage than they did three years ago, signing an instrument that hands an additional pressure point to an investor is a structural decision worth making deliberately rather than by default.

The ASA: the UK-specific instrument most founders underuse

The Advance Subscription Agreement, or ASA, is the instrument that most UK founders should be reaching for first and most are not. ASAs are popular in the UK because of their compatibility with the Seed Enterprise Investment Scheme and Enterprise Investment Scheme, which offer significant tax relief to investors who fund qualifying companies. That compatibility is not a technicality. It is a meaningful commercial advantage that affects the pool of investors available to you and the effective cost of capital you are raising.

SEIS and EIS relief allows qualifying UK investors to claim back a significant portion of their investment as income tax relief, reducing their effective risk on the downside while maintaining full upside participation. For early-stage UK angels, many of whom are private individuals investing from their own capital, that tax relief is often a determining factor in whether they invest at all and at what valuation they are willing to invest. A founder raising on an ASA is offering something a SAFE cannot: a structure that makes the investment more attractive to the UK angel market at no additional cost to the founder.

The mechanical difference between an ASA and a SAFE at conversion is, in most standard scenarios, negligible. Both are not debt instruments. Neither accrues interest. The investor’s ownership is fixed at signing based on the investment amount and the valuation cap, and that ownership converts into shares at the next priced round on substantially similar terms. In the scenario we modelled, the SAFE and ASA produce identical post-Series A outcomes: 68.9% founder ownership, 6.89% to the early investor.

The ASA and the SAFE arrive at the same place. The difference is that the ASA gets you there with a broader pool of UK investors willing to come on the journey, because the tax relief makes the risk more manageable for them.

The one structural difference worth understanding is that ASAs are typically designed around a qualifying funding round trigger rather than any priced round. The investment converts when a round that meets specific criteria closes, usually a minimum raise amount or a particular investor type. That trigger is worth reading carefully in the document, because a round that does not meet the qualifying criteria may not trigger conversion, which creates ambiguity that a well-drafted SAFE avoids.

Which instrument should you be using

For most UK pre-seed founders raising from UK angels, the answer is an ASA. It produces the same economic outcome as a SAFE at conversion, carries no interest, has no maturity date, and is compatible with SEIS and EIS relief in a way that makes it meaningfully more attractive to the investor base you are most likely to be raising from. The legal cost of drafting one is comparable to a SAFE, and the commercial advantage of SEIS and EIS compatibility is real enough that defaulting to a US-style SAFE without considering it is leaving something on the table.

A convertible note is the right instrument in specific circumstances: when an investor requires it, when you are raising a bridge round from existing institutional investors who have convertible note infrastructure in place, or when the legal framework of a particular raise makes debt treatment preferable. It is not the right default for a UK pre-seed raise from angels, and the maturity date risk in a market where Series A timelines are extending is a structural disadvantage that compounds if the fundraising environment deteriorates.

The SAFE remains valid, particularly if you are raising from US investors or investors familiar with Y Combinator’s standard documents who prefer its simplicity and enforceability. In a cross-border raise, or a raise where investor familiarity with the instrument matters for closing speed, a SAFE is a reasonable choice.

The decision is not primarily about the conversion mechanics, which as we have shown are nearly identical across all three instruments when the cap is binding. It is about the obligations you are taking on between signing and conversion, the investors you are making the instrument attractive to, and the structural position you want to be in if the timeline to your next round is longer than you planned for.

At RoundRaise, we build tools that help founders model the conversion outcomes of different instruments before they sign. If you want to run the numbers on your own raise across SAFE, convertible note, and ASA scenarios, you can find us at roundraise.co.uk.

We also have a founder wall at app.roundraise.co.uk/board, a space where founders leave the things they wish they had known earlier. If you have been through a raise and have something worth leaving there, we would be glad to have it.