The Term Sheet Decoded

20 May 2026 · 11 min read

Milan Bilimoria

Milan BilimoriaA term sheet is not a formality. It is the document that determines your financial outcome at exit, your negotiating position at every subsequent round, and in some cases whether you walk away from the company you built with anything meaningful at all. Most founders treat it as the final step before the money arrives. The ones who negotiate well treat it as the moment the real work begins.

The terms that matter most are rarely the ones that get the most attention. Valuation and round size are the numbers that dominate founder conversations about term sheets, but they are also the numbers both parties understand going in. It is the structural terms, the ones that sit in dense clauses below the headline economics, that consistently produce outcomes founders did not anticipate when they signed.

Based on analysis of UK seed term sheets and conversations with founders who have been through the process, here are six terms worth understanding before you get to the room, what each one does financially, and what a good outcome looks like for each.

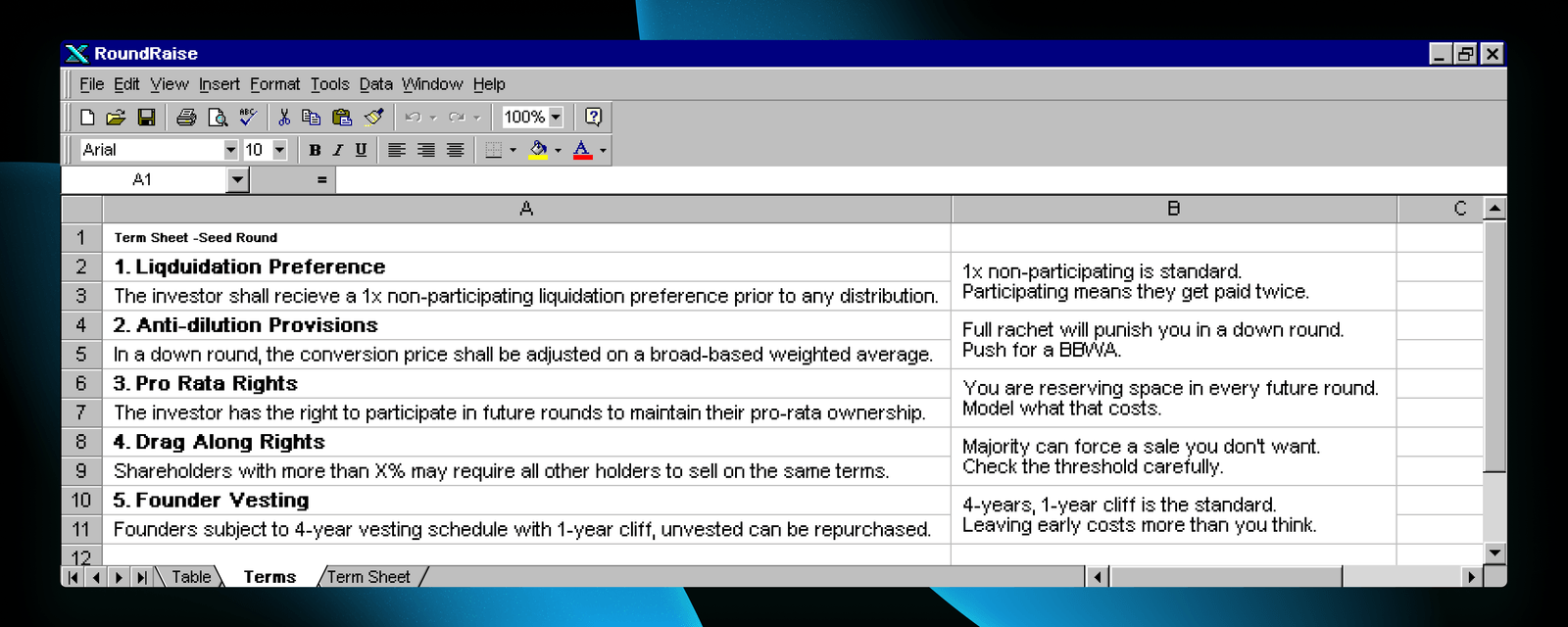

1. Liquidation preference

We have covered this in detail in a previous piece, but it belongs on this list because it is the term with the most direct impact on founder proceeds at exit and the one most commonly misread.

The market standard in the UK is a 1x non-participating liquidation preference, which means the investor receives their original investment back before any proceeds are distributed to other shareholders, and then chooses between taking that preference or converting their shares and participating pro rata in the full exit proceeds. They will always choose whichever returns more. Below a certain exit valuation they take the preference; above it they convert. That structure is genuinely founder-friendly because the investor gets one bite, not two.

A participating preference changes that entirely. The investor takes their original investment back first and then participates pro rata in what remains alongside all other shareholders. They get paid twice: once from the preference stack and once from the distribution. At modest exit valuations, the difference between a participating and non-participating structure can amount to seven figures in founder proceeds.

When you see a participating preference in a term sheet, it is negotiable. The market standard exists for a reason, and a well-advised investor knows that pushing for participating preferences at seed is an aggressive ask in the current UK market. Push back with reference to market standard and have your lawyer do the same.

2. Anti-dilution provisions

Anti-dilution provisions protect an investor’s ownership percentage if the company subsequently raises capital at a lower valuation than the current round, a scenario known as a down round. The provision works by adjusting the price at which the investor’s preferred shares convert into ordinary shares, giving them more shares at conversion than they originally received, which compensates them for the valuation drop.

There are two versions of this term and the difference between them is significant. Broad-based weighted average anti-dilution adjusts the conversion price based on a weighted average of the old and new share prices, taking into account all shares outstanding. The adjustment is proportional to the size of the down round and the number of new shares issued, which means a small down round produces a modest adjustment and a large one produces a more significant one. This is the market standard in the UK and it is the version founders should be pushing for.

Full ratchet anti-dilution is the aggressive version. It adjusts the conversion price to match the new lower price per share in the down round, regardless of how many shares were issued at the lower price or how small the down round was. In practice, a single share issued at a lower valuation triggers the full ratchet for the entire investor position, which can produce a dramatic and disproportionate dilution of the founder’s ownership. Full ratchet provisions are rare in UK seed term sheets but they do appear, and a founder who signs one without understanding it is accepting a term that could be severely punishing if the company goes through a difficult period before its next raise.

The ask is straightforward: broad-based weighted average is market standard, full ratchet is not, and you should not accept it without significant concessions elsewhere in the term sheet.

3. Pro rata rights

Pro rata rights give an investor the right to participate in future funding rounds to maintain their ownership percentage. If you raise a Series A and your seed investor has pro rata rights, they are entitled to invest enough in the Series A to keep their stake from being diluted below its current level. From the investor’s perspective this is a straightforward protection of their position in a company they have already backed. From the founder’s perspective it is a commitment that deserves more careful thought than it typically receives.

The financial consequence of pro rata rights is not felt at the current round but at the next one. When a Series A investor is allocating the round, they are working with a fixed total raise amount. If existing seed investors are exercising pro rata rights and taking up a meaningful portion of that allocation, the amount available to the Series A lead and other new investors is reduced. In a competitive round where multiple investors want to participate, that constraint can create friction. In a round where you are trying to bring in a specific strategic investor, it can limit your flexibility to allocate to them.

Pro rata rights are standard and you will almost certainly grant them to your lead investor. The question worth asking is whether you are also granting them to every angel and small investor in the round, because the cumulative effect of many investors each exercising modest pro rata rights can become a meaningful constraint on future round structure. Consider whether pro rata rights should be limited to investors above a certain cheque size threshold, which is a reasonable and increasingly common ask in UK seed rounds.

4. Drag along rights

Drag along rights allow a majority of shareholders to compel all other shareholders to sell their shares in the event of an acquisition or other exit. The purpose is to prevent a minority shareholder from blocking a sale that the majority, including the founder and the lead investor, have agreed to. In that framing, drag along rights are a sensible mechanism: a single angel holding a small stake should not be able to veto an exit that everyone else wants to proceed with.

The term becomes more consequential when you examine the threshold that triggers it and who counts toward that majority. A drag along provision triggered by shareholders holding 50% of the company sounds straightforward until you consider that in some cap table structures, a combination of investors holding preferred shares could constitute a majority without the founder’s participation. In that scenario, the drag along could theoretically be used to force a sale that the founder opposes.

The number to pay attention to in the term sheet is the threshold percentage required to trigger the drag along, and whether ordinary shares and preferred shares are counted separately or together in calculating that threshold. A well-constructed drag along provision requires the consent of both the majority of ordinary shareholders and the majority of preferred shareholders, which effectively gives the founder a veto as the largest ordinary shareholder. If the provision in your term sheet does not include that protection, it is worth negotiating before you sign.

5. Founder vesting

Founder vesting provisions require founders to earn their shares over a period of time rather than owning them outright from day one. The standard structure in UK seed rounds is a four year vesting schedule with a one year cliff, meaning no shares vest in the first twelve months, 25% vest at the end of month twelve, and the remaining 75% vest monthly over the following three years. According to data from UK seed term sheets, vesting provisions appear in 65% of seed stage deals, making them the norm rather than the exception.

The financial consequence of founder vesting is most visible when a founder leaves the company before their shares are fully vested. If you leave after eighteen months on a four year schedule, you have vested 37.5% of your shares and forfeited the remaining 62.5% back to the company. For a founder who holds a significant equity stake, that forfeiture can represent a substantial financial loss, and it is a scenario worth modelling before you sign rather than after.

Two things are worth negotiating in the vesting clause. The first is acceleration: a provision that allows some or all of your unvested shares to vest immediately upon a change of control, meaning an acquisition. Without acceleration, a founder who sells their company two years into a four year vesting schedule may find that half their equity does not vest at exit, which is a significant and often unexpected reduction in proceeds. Single trigger acceleration, which vests shares on acquisition alone, is more founder-friendly than double trigger, which requires both acquisition and termination. The second is whether any credit is given for time already spent building the company before the investment closes, which is a reasonable ask if you have been working on the business for a significant period pre-funding.

6. Founder leaving provisions

Founder leaving provisions, sometimes called good leaver and bad leaver clauses, determine what happens to a founder’s shares if they leave the company after the investment closes. They appear in 59% of UK seed term sheets and are among the least understood terms in the document, partly because they sit in a section most founders do not expect to be relevant to them and partly because the language tends to be dense enough that the financial consequence is not immediately obvious.

The distinction between a good leaver and a bad leaver is not always intuitive. A good leaver is typically a founder who leaves for reasons outside their control: serious illness, death, or dismissal without cause. A bad leaver is a founder who leaves voluntarily, is dismissed for cause, or breaches their obligations to the company. The financial difference between the two classifications is significant. A good leaver typically retains their vested shares and may receive fair market value for their unvested ones. A bad leaver typically forfeits their unvested shares and in some cases is required to sell their vested shares back to the company at cost, meaning the price originally paid for them rather than their current market value.

The term worth scrutinising is the definition of bad leaver, because it varies considerably across term sheets and the consequences of being classified as one are severe. A definition that includes voluntary resignation as a bad leaver scenario means that a founder who chooses to step back from the business for any reason, even years into building it, may be required to sell their vested shares back at cost. That is a punishing outcome for a founder who has contributed significantly to the company’s value, and it is worth negotiating a narrower definition before the term sheet is signed. At minimum, push for voluntary resignation after a certain period of service to be treated as a good leaver event, or for vested shares to be exempt from the bad leaver provisions entirely.

None of these terms are exotic. They appear in the majority of UK seed term sheets and they have been standard features of venture investment documents for long enough that most investors will tell you they are non-negotiable market standard. Some of them are. Some of them are not, and the ones that are not tend to be the ones that matter most when something unexpected happens to the company or to you personally.

The ask is not that you reject every term that is not maximally founder-friendly. It is that you understand what you are signing before you sign it, model the financial consequence of each clause at the scenarios that are realistic for your company, and negotiate from a position of clarity rather than relief that the term sheet arrived at all.

At RoundRaise, we build tools that help founders understand the financial structure of their round before they commit to it. If you are working through a term sheet or want to model the cap table consequences of specific terms, you can find us at roundraise.co.uk.

If this was useful, subscribe below — we publish one piece like this every week.