The Term You Signed Without Modelling

6 May 2026 · 7 min read

Milan Bilimoria

Milan BilimoriaWe've spent time speaking with seed investors and angels about what actually happens when a founder's cap table lands in front of them. But this piece is about something different: not what investors see, but what you agreed to, and what it means when the company you built finally sells

Most early-stage founders understand liquidation preferences in roughly the same way. The investor gets their money back first. Whatever’s left goes to everyone else. That framing is not wrong, but it is incomplete in a way that matters enormously when exit proceeds are being distributed, and it misses the distinction that determines whether the term you signed was founder-friendly or not.

There are two versions of a liquidation preference that you are likely to encounter in a UK seed or Series A term sheet. Both are called liquidation preferences. Both use the same language in the same section of the same document. But they produce meaningfully different outcomes for your proceeds at exit, and the difference between them is a single word: participating.

Understanding what that word does mechanically is not a legal exercise. It is a financial one, and it is worth doing before you sign rather than after.

What the standard term actually says

The market standard in the UK is a 1x non-participating liquidation preference. In 2025, 90% of preference shares in the UK were non-participating, and 96% of those carried a 1x multiple. That means the vast majority of institutional investors in the UK are using this structure, and if your term sheet reflects market standard, this is what you are signing.

Here is what it means in practice. When a liquidity event occurs, whether that is an acquisition, a sale, or a winding up, the investor with a 1x non-participating preference has a choice. They can either take back their original investment amount before any proceeds are distributed to other shareholders, or they can convert their preferred shares into ordinary shares and participate in the proceeds pro rata alongside everyone else. They will always choose whichever option returns more money to them.

At a modest exit, where the total proceeds are not dramatically higher than the post-money valuation of the round, the investor will typically take the preference. At a larger exit, where the proceeds are high enough that their pro rata share of the total exceeds their preference, they will convert. The crossover point is straightforward to calculate: it is the exit valuation at which the investor’s pro rata ownership percentage multiplied by the total proceeds equals their preference amount. Below that point they take the preference; above it they convert.

This structure is genuinely founder-friendly in the sense that it protects the investor’s downside without allowing them to extract disproportionate returns at every exit size. The investor gets one bite, not two.

What a participating preference does instead

A 1x participating liquidation preference removes that choice. The investor takes their original investment back first, and then participates pro rata in the remaining proceeds alongside all other shareholders. They get both the preference and the participation. There is no conversion decision because there is no trade-off to make; the structure is designed to give the investor their capital back and a share of the upside regardless of exit size.

At seed level in the UK, participating preferences doubled from 7% to 14% in 2025, which means they remain a minority term but a growing one. They are more common in rounds where the investor has significant leverage, where the founder has fewer competing term sheets, or where the round has taken longer to close than anticipated and the founder has accepted more structured terms in exchange for getting the deal done.

The practical consequence of a participating preference is that the investor is extracting value from two places simultaneously at exit: from the preference stack and from the pro rata distribution. Every pound they take from the preference stack is a pound that does not reach the pro rata pool; and every share they hold in the pro rata pool is a share that reduces what you receive from the remaining proceeds. At modest exit valuations, the combination of these two effects produces a materially different outcome for founder proceeds than the non-participating equivalent.

What the numbers look like in practice

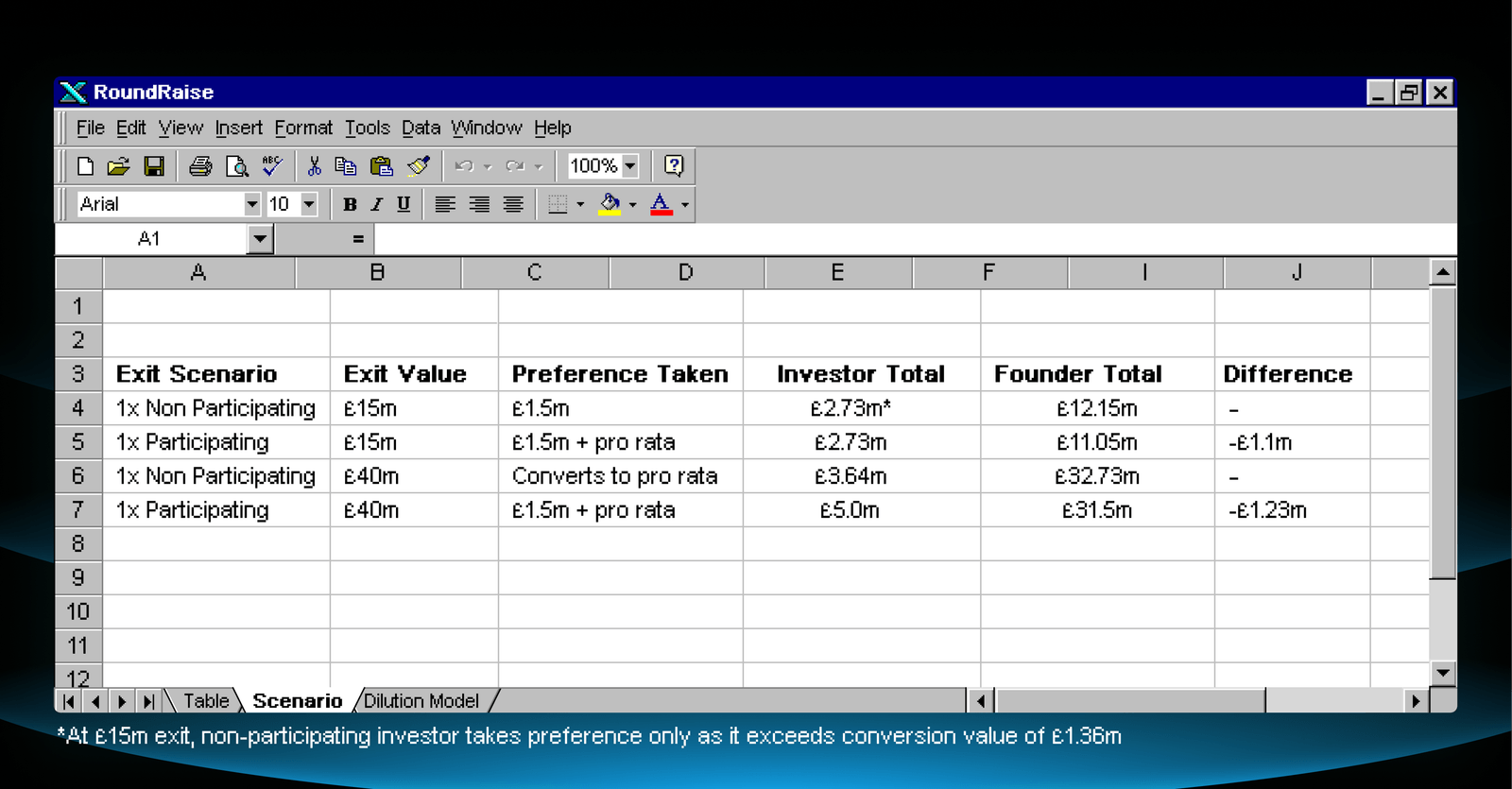

To make this concrete, consider a realistic scenario for a UK early-stage founder. You have raised a £1.5m Series A at a £15m pre-money valuation, giving the investor 9.09% of the company post-money. A 10% option pool has been created pre-money at Series A, which you have absorbed, leaving you with 81.82% of the company. The rest is held by the option pool and other minor shareholders.

Two years later, the company sells. Here is what your proceeds look like under each structure at two different exit valuations.

At a £15m exit, the difference between the two structures is £1.1m in your pocket. The investor under a participating structure takes their £1.5m preference and then a 9.09% share of the remaining £13.5m, totalling £2.73m. Under a non-participating structure, they take their preference only, leaving you with £12.15m rather than £11.05m.

At a £40m exit, the gap is £1.23m. Under non-participating, the investor converts their preference and takes their pro rata share of the full proceeds; under participating, they take the preference and their pro rata share of what remains after it, which produces a higher total return for the investor and a lower one for you.

The gap narrows as exit size increases, which is why participating preferences feel less threatening when you are modelling optimistic scenarios. At a £200m exit the difference is proportionally small. But most UK seed-stage companies that exit do not exit at £200m. The exits that are most likely for your ICP are also the exits where the structure of this term has the most impact on what you actually receive.

Why this matters before the round closes, not after

The reason liquidation preferences deserve more attention from early-stage founders than they typically receive is that by the time they matter, it is too late to do anything about them. The term is agreed at the point of investment. It sits in the shareholder agreement, largely invisible across the years of building that follow, and surfaces only when proceeds are being distributed. At that point, the calculation is mechanical; there is no negotiation, no context to provide, no argument to make about what you intended when you signed.

If a founder hasn’t done their waterfall modelling, doesn’t know what to look out for, and hasn’t appreciated the risks embedded in the deal structure, that can leave them receiving a payout far less than they expected.

The ask is not that you reject every term sheet with a participating preference, though you should negotiate hard against them when you have the leverage to do so. The ask is that you model it before you sign. Run the exit waterfall at three or four different exit valuations. Understand what the investor receives and what you receive under each scenario, and make the decision to accept or negotiate the term with full visibility of its consequences rather than a general sense that it is probably fine.

A liquidation preference is not an administrative detail in a term sheet. It is one of the most direct determinants of your financial outcome at the moment the company you built changes hands. It deserves to be treated accordingly.

At RoundRaise, our cap table tool models exit waterfalls across different liquidation preference structures, so you can see exactly what you and your investors receive at any exit valuation before you sign. If you are working through a term sheet or want to stress-test your current structure, you can find us at roundraise.co.uk.

If this was useful, subscribe below, we publish one piece like this every week.

Subscribe